Today is the first day back to work in the Year of the Tiger, wishing everyone a prosperous Year of the Tiger and may your wealth multiply like the tiger adds to it!

During the holiday, besides spending time with family, visiting relatives and friends, and exercising, I managed to dedicate about 30 hours to organizing some events and my thoughts on carbon neutrality from 2021, as well as my reflections and judgments for the future, writing this article titled China's Carbon Neutrality 2.0.

The reason why this article is named as such is because around this time last year, I wrote an article called China's Carbon Neutrality. A year has passed, and China's carbon neutrality development has been rapid, quickly breaking through the circle and gaining public recognition and approval, gradually becoming a clear card for the next 40 years. The goal of China's carbon neutrality has been repeatedly mentioned by national leaders (according to incomplete statistics, President Xi Jinping has mentioned carbon neutrality more than 34 times at various international and domestic conferences, and each mention has been firmer and more specific). The overall progress of carbon neutrality has far exceeded most people's expectations, moving from initial neglect to today's universal discussion.

The reason for choosing China's Carbon Neutrality 2.0 instead of 1.01 or 1.1 is, firstly, because I have a background in programming and am accustomed to using numbers like 1.0, 1.1, 2.0, etc., to represent version numbers; secondly, because the development progress of China's carbon neutrality in 2021 truly deserves a major version upgrade.

2021 was the inaugural year of China's carbon neutrality, and the carbon neutrality of 2021 was magical, noisy, and phenomenally impactful, even leading to overly aggressive carbon reduction movements. We need to settle down, think deeply, and upgrade rationally. 2022 will be the year of breakthrough actions for China's carbon neutrality. I hope that combining the observations and discoveries of Carbonstop's team and myself in the field of carbon neutrality over the past year, as well as practical experience in corporate carbon neutrality, can contribute to the advancement of China's carbon neutrality process and provide some reference and assistance to enterprises and institutions that wish to engage in carbon neutrality in China. This article will mainly discuss the following topics:

01 Upgrading the Definition of Carbon Neutrality

02 Upgrading the Internal Driving Force of Chinese Enterprises' Carbon Neutrality

03 The Official Launch of China's Carbon Trading

04 Upgrading the Pathway to Corporate Carbon Neutrality

05 To Investors in the Carbon Neutrality Field: Predictions for the Future of Carbon Neutrality

06 To Friends of Carbonstop (Partners, Clients, and Future Investors)

07 Imagining What a Carbon Neutral Enterprise Looks Like

[Upgrading the Definition of Carbon Neutrality]

The breakout of carbon neutrality into mainstream awareness is evident. Here is a personal experience: recently, I interviewed many IT engineers (who had no prior connection with carbon neutrality), and as the final round, I would ask candidates if they understood carbon neutrality and their take on it. Surprisingly, recent IT engineer candidates have a fairly good understanding of carbon neutrality (most can explain the logic behind carbon neutrality and why China needs to pursue it), even surpassing some carbon consultants who applied to our company around this time last year. This indicates a significant improvement in societal understanding and recognition of carbon neutrality.

The latest Chinese definitions of carbon neutrality on Baidu Baike and Wikipedia are also more accurate and complete, aligning with the definition provided by Carbonstop's team at the beginning of last year:

Carbon neutrality refers to the total amount of carbon dioxide or greenhouse gas emissions directly or indirectly produced by a country, enterprise, product, activity, or individual within a certain period, which is offset through measures such as afforestation and energy conservation and emission reduction, achieving positive and negative offsets, reaching relative "zero emissions."

The main difference from the previous version of Baidu Baike is that the scope of carbon neutrality has been upgraded, expanding to cover countries, enterprises, products, activities, and even individuals. Indeed, the progress of carbon neutrality in the past year has verified this point. In addition to countries and enterprises, examples of carbon-neutral products, green meetings, and personal carbon neutrality have emerged one after another.

★ Product Carbon Neutrality

After launching the Carbon Cloud SaaS product on September 22, 2021, the best-selling module was the product carbon footprint module. More and more enterprises are not only concerned about how much carbon emissions their company generates annually but also start paying attention to whether their products meet national and international requirements for product carbon neutrality/carbon disclosure, indicating that companies are beginning to focus on improving their product carbon footprints. For example, ZhenGu's carbon-neutral chocolate, KFC's carbon-neutral oat milk, SKP's carbon-neutral mineral water, and so on. An increasing number of products are paying attention to carbon footprints and carbon neutrality, and we expect to see more carbon-neutral products in 2022.

★ Event Carbon Neutrality

In terms of event carbon neutrality, there have been many encouraging phenomena. Most companies have started to try light-weight models of green meetings to practice their carbon neutrality. I know of no fewer than 100 carbon-neutral green meetings that have been realized, such as:

2021 National Energy Group Hydrogen Conference

2021 World New Energy Vehicle Conference

2021 International Energy Internet Conference

2021 ByteDance's Giant Engine Conference

2021 Zhizhu High-tech Zone Sustainable Development Forum

......

★ Personal Carbon Neutrality

Achieving carbon neutrality at the national level cannot be done without the efforts and contributions of every individual. Personal carbon neutrality has also become a trend. Vanke recently conducted personal carbon neutrality for its main partners and leaders, although it is currently done through a relatively simple method of purchasing CCERs, and uniformly according to a standard of 7 tons of carbon emissions per person for offsetting, with many details that can still be upgraded (for example, whether the carbon footprint generated by each person can be calculated more precisely, considering the main areas of clothing, food, housing, transportation, and use in their lives; whether the aspects of carbon emissions reduced by each person for society can be reflected before proposing methods of offsetting).

However, taking this first step is very meaningful for the progress of personal carbon neutrality in China. It is believed that by this time next year, more responsible individuals will be willing to understand their own carbon footprint and achieve their own carbon neutrality through reducing emissions and offsetting methods.

According to Carbonstop's team analysis of the potential for low-carbon consumption among residents of large cities, in 2020, through small efforts, each person could achieve a carbon reduction of about 1 ton per year. By 2030, each person could reduce carbon emissions by 2 tons per year. If this data is scaled up to the national and global levels (assuming the world's total carbon emissions are about 55 billion tons annually, and the population reaches 10 billion, assuming urbanization is largely completed by 2030, the carbon reduction achieved through individual efforts could approach 20 billion tons, even halved, it could contribute 10 billion tons of carbon reduction), this would be of great significance for advancing the global response to climate change.

[Upgrading the Internal Driving Force of Chinese Enterprises' Carbon Neutrality]

Even today, most people (including the thousands of carbon neutrality-related companies established in the past year or so) basically believe that government control of high-energy-consuming enterprises and carbon trading is the only or primary path to China's carbon neutrality. Through observations and practical experiences over the past year, I found that the internal driving force for Chinese enterprises to engage in carbon neutrality has undergone a significant upgrade, shifting from passive to proactive. Not only regulated enterprises but also more brand enterprises, and even manufacturing enterprises, are actively making efforts on this trillion-dollar, epic golden track of carbon neutrality.

Tech companies, Tencent proposed its own carbon neutrality pathway on January 12, 2021 (although it has not yet set specific emission reduction targets); Baidu committed to carbon neutrality by 2030 in June last year and disclosed its carbon emission data (becoming the first tech company to disclose its own carbon emission data); Alibaba also disclosed its carbon neutrality goals and creatively proposed Scope 3+. The targets set by these leading tech companies are not aligned with China's carbon neutrality goals or the actions of domestic companies, but rather with the actions of the world's top tech companies in carbon neutrality.

Among consumer brands, Starbucks launched a carbon-reducing sandwich made from plant-based meat; KFC introduced carbon-neutral oat milk (calculated the full lifecycle carbon footprint and achieved product carbon neutrality through carbon sink projects); SKP announced in November 2021 that it has become China's first carbon-neutral retail mall. The actions of brand carbon neutrality are getting closer to every consumer.

L'Oréal has committed to achieving full carbon neutrality across its facilities by 2025 and to reducing absolute Scope 1, 2, and 3 emissions by 25% by 2030 compared to 2016, including Scope 3 emissions, meaning L'Oréal is inviting (Yao) its suppliers to also gradually achieve carbon reduction or carbon neutrality. For example, Huaxi Biotech, as a supplier to L'Oréal, faces direct demands from L'Oréal for carbon disclosure and reduction. To secure orders, especially from major clients, supplier companies can make all-out efforts. Of course, Huaxi Biotech is already a large company, there are hundreds of thousands, even millions, of supplier companies similar to Huaxi Biotech in China, and these companies are facing or will soon face requirements from downstream brand clients regarding organizational carbon emissions and product carbon footprints, which is the true driving force behind Chinese enterprises achieving carbon neutrality.

The driving force for brand companies (such as Starbucks, Apple, SKP, KFC, Adidas, L'Oréal, etc.) lies in being the first to launch carbon neutrality goals and pathways to win the favor of more consumers. Taking Apple as an example, ten years ago, the killer feature of Apple's iPhone products was their powerful functions and stunning design, winning the affection of countless consumers and their willingness to pay a premium price.

But in recent years, with competitors gradually catching up, to be honest, the competitiveness of iPhones in terms of functionality and design has gradually diminished. To win the new competition, Apple CEO Tim Cook always emphasizes how the new generation of iPhones reduces the carbon footprint to win consumers' loyalty to the brand and their long-term support, achieving very good results.

Carbon neutrality has evolved from an external image factor to a core competency driving the development of the main business of enterprises. And Apple has announced that by 2030, all its suppliers and products will achieve carbon neutrality, which sets new competitive requirements for the entire supply chain, including peers Huawei, Samsung, Lenovo, Xiaomi, and suppliers Foxconn, BOE, and others.

For China's manufacturing sector, many enterprises are also facing the requirement of the EU and US border carbon tax:

"In March 2021, the European Parliament adopted the resolution on the EU Carbon Border Adjustment Mechanism (CBAM), planning to levy a carbon tariff. Once the carbon tariff is officially implemented after 2023, the EU will impose taxes on the carbon content of imported goods. Based on the mechanism of calculating the carbon tariff according to the difference between the EU carbon price and the carbon prices of other countries or regions, international carbon markets are expected to gradually connect in the future, and carbon prices in different countries and regions are expected to converge, which would also lead to an increase in China's carbon prices."

"On July 19, 2021, The New York Times reported that the U.S. Democrats would soon announce a plan under which the United States would introduce a new 'carbon border tax' aimed at taxing imports from China and other countries that do not significantly reduce their global warming pollution. Preliminary estimates suggest that the Democratic Party's proposal, if supported by the U.S. Congress and implemented, would generate $16 billion in border tax revenue annually. The core and most detrimental factor to China in the Democratic Party's proposal is that its tax base is the total greenhouse gas emissions of the country of origin of the imported products, rather than per capita carbon emissions."

Setting aside political factors at the national level and nationalism, the policy information above has a direct and fast impact on Chinese enterprises. From the practical experience of my team, many companies in certain industries, such as the recycled plastics industry, have already faced direct constraints from the EU's border carbon tax. Chinese plastic products exported to the EU must ensure that at least 30% of the material is recycled plastic, posing a new challenge to China's manufacturing sector. Understanding the recycled plastic content and carbon footprint of each product has become a necessity!

Of course, in addition to external pressures, there must also be internal motivation. The recent launch of the carbon emission reduction support tool by the People's Bank of China has gradually taken effect. Enterprises that make contributions in the field of carbon emission reduction can obtain low-interest loans from commercial banks, and this incentive policy will bring significant benefits and profound implications for Chinese enterprises' carbon neutrality. My team has recently begun participating in some commercial banks and credit information platforms in the assessment of carbon reduction volumes for corporate carbon reduction projects, proving that this policy has truly begun to take root.

In summary, the external pressures and internal motivations for Chinese companies to achieve carbon neutrality have gradually come to light and are visibly impacting their business operations.

Overall, the driving forces behind Chinese companies' pursuit of carbon neutrality have undergone significant changes, moving beyond traditional high-emission, high-energy-consuming industries to penetrate all sectors of society. Carbon neutrality is an open card, based on this open card, how companies play their hand is promising!

【China's Carbon Trading Finally Kicks Off】

Research indicates that China’s commitment to carbon neutrality could prevent a global temperature rise of 0.2°C - 0.3°C, with China's carbon trading incorporating 4.5 billion tons of carbon emissions, accounting for more than 40% of the country's total carbon emissions. The smooth implementation of China's carbon trading will have a significant positive impact on global efforts to combat climate change.

Speaking of China's national carbon trading, it can be described as "long-awaited." Announced on December 19, 2017, China's carbon trading market did not begin actual transactions until July 16, 2021, a process that was complex and arduous, one that not everyone or every institution could endure.

Overall, the first carbon trading compliance cycle concluded relatively smoothly. By the end of December 31, 2021, the cumulative trading volume of carbon emission allowances reached 179 million tons, with a cumulative trading value of 7.661 billion yuan, and an average transaction price of 42.85 yuan per ton, achieving a compliance rate of 99.5% (by compliance quantity). The basic framework of the national carbon market has been preliminarily established, the role of the price discovery mechanism has begun to show, and the awareness and capability levels of enterprises in reducing emissions have been effectively improved, promoting the reduction of greenhouse gases and accelerating the green and low-carbon transition of enterprises.

Discussing observations over the past year, issues within China's carbon market that were previously emphasized by industry peers have gradually become exposed and optimized, such as the problem of carbon emission data fabrication by controlled emission enterprises which received unprecedented attention and handling; the chaos where entities both acted as referees and players in carbon verification has seen some institutions proactively step forward to clarify, all of which positively push for the purification and long-term healthy development of the carbon trading market.

The author's greatest impression recently is that more and more institutions are buying carbon, some for their own carbon neutrality, needing to purchase CCERs or forest carbon sinks, others for carbon trading compliance due to quota shortages, which has driven up carbon prices, including previously three-category CCER projects that could only sell for a few yuan now fetching nearly 60 yuan, demonstrating the market's heat. Of course, the author believes that current carbon trading does not yet truly reflect the cost of corporate carbon reduction, and prices may continue to rise with the enthusiasm for corporate carbon neutrality, although they will also fluctuate cyclically with the carbon market's compliance cycles. There is no doubt that carbon will become a scarce resource in the near future (or even now).

Another phenomenon is that large state-owned enterprises (SOEs) and central SOEs, such as some major energy groups emitting several hundred million tons, even close to one billion tons, whose every move can even affect global temperature changes (according to the above forecast, if a certain energy group achieves carbon neutrality, the world could potentially see a 0.02-degree decrease in temperature). Due to the numerous enterprises within these groups participating in carbon trading, how to allocate resources internally at the lowest cost to fulfill carbon trading compliance has become a trend, and the construction of intelligent carbon emission and carbon trading management software systems has become a standard configuration for most carbon trading enterprises.

【Upgrading the Corporate Carbon Neutrality Path CREO】

In 2021, the global corporate carbon neutrality process accelerated, and my team, while working on projects, also analyzed the carbon emission calculations and carbon neutrality action plans of major global companies, especially tech firms.

Around this time last year, Carbonstop creatively proposed the Corporate Carbon Neutrality Path CREO methodology (for details, please refer to [Carbonstop Original] China's Carbon Neutrality), which received positive feedback from the industry, including Starbucks, Hillhouse Capital, Nenglian, SKP, Baidu, and others adopting CREO or similar methods to plan their carbon neutrality paths.

After a year of rapid development, many companies on the path to achieving carbon neutrality have started to encounter new challenges and propose new ideas. I will analyze in detail from the perspective of the CREO path.

★Calculating(Calculation):

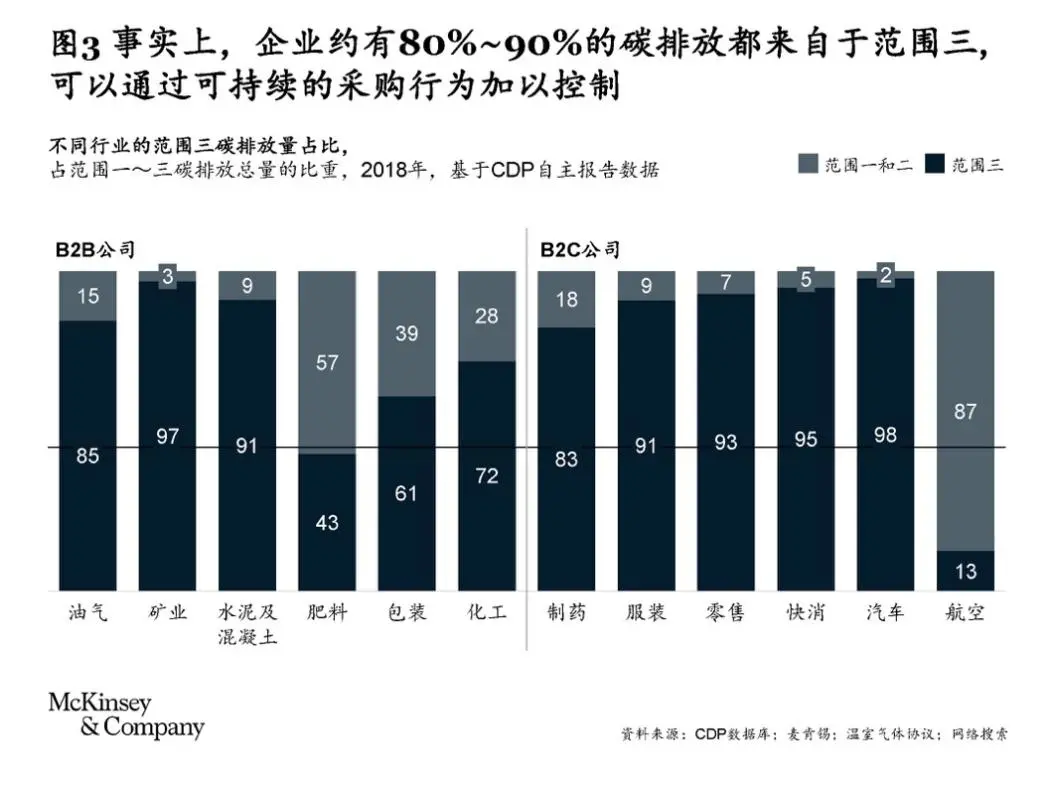

A necessary step for companies to achieve carbon neutrality is to calculate their carbon emissions across various dimensions. In the core content of carbon emission calculation, many companies are no longer satisfied with calculating emissions at the organizational level; they are beginning to attempt to calculate the full lifecycle carbon footprint of their products and services, tracing the carbon footprint up and down the supply chain. Because what consumers buy are not the companies themselves but the products or services produced by the companies, they hope to understand the carbon footprint or environmental impact of each product or service when making purchasing decisions; many companies are also no longer satisfied with just calculating Scope 1 & 2 & 3 emissions, they are beginning to explore calculating Scope 4 or Scope 3+ emissions, which are very positive phenomena.

In terms of carbon disclosure, the latest news is that the California Senate has passed a bill requiring companies doing business in California with annual revenues exceeding $1 billion to disclose all scopes of carbon emissions annually, including direct emissions (Scope 1), emissions from purchased and used electricity (Scope 2), and indirect emissions, including those from the company's supply chain (Scope 3) (see: California Senate passes bill requiring companies to disclose all greenhouse gas emissions (including Scope 3)

I believe that the calculation and disclosure of Scope 3 emissions will soon become a necessity (not immediately requiring companies to disclose all 15 categories of Scope 3 emissions, but encouraging companies to disclose as comprehensively as possible the Scope 3 carbon footprint), and the disclosure of Scope 4 or Scope 3+ should be advocated and encouraged, and institutional design should provide certain spiritual and material rewards to companies that voluntarily disclose Scope 4 or Scope 3+ emissions.

An important change is: the international standard for corporate carbon accounting ISO14064-1:2018 edition will be fully implemented before June 2022, and the previous ISO14064-1:2006 edition will no longer be allowed. The biggest change in the 2018 edition compared to the 2006 edition is the abandonment of the internationally common Scope 1 & 2 & 3 terminology in favor of the six categories of greenhouse gas emissions (but the overall coverage remains consistent with Scope 1 & 2 & 3):

- Direct emissions or removals

- Energy indirect emissions

- Transportation indirect emissions

- Indirect emissions from purchased products or services

- Downstream supply chain indirect emissions

- Other indirect emissions

This means that the commonly accepted terminology of Scope 1, 2, and 3 will be replaced.

★Reducing(Reduction):

When companies set out their carbon neutrality paths, there is a general international consensus against the approach of wealthy companies simply throwing money at carbon neutrality. My team always encourages and guides companies to reduce emissions as much as possible, and only resort to offsetting for unavoidable emissions to achieve carbon neutrality. However, how much is enough to reduce emissions? What is considered reasonable? There is no unified answer internationally. 【This issue welcomes your comments and discussion, and the top 5 heartfelt commenters in 2022 will receive a free learning opportunity organized by Carbonstop Academy】

I believe this requires a balance point, i.e., companies can consider buying carbon credits if the cost of their own carbon reduction efforts is indeed higher than the cost of buying carbon. Therefore, when setting their carbon neutrality path, companies need to clearly explain the relationship between reduction costs and carbon prices, along with relevant evidence. If choosing to buy carbon, it is also necessary to trace whether each penny spent truly contributes to social carbon reduction, and regular reviews and reports are essential.

If the above methods are operationally challenging or costly, I recommend a relatively simple and feasible way: companies prove that their reduction volume exceeds the amount of carbon credits purchased, which makes them less likely to face challenges.

Here, I would like to briefly respond to the viewpoint of numerous NGOs regarding the "greenwashing" issue (here referring only to carbon emission indicators, not other environmental indicators) mentioned earlier. Combining the above analysis, if a company can prove its efforts in emission reduction are significant (such as investing more in reduction costs than buying carbon, and having a relatively lower carbon intensity in the industry), then the company can largely avoid being accused of "greenwashing."

★Engaging(Engagement):

More and more companies are not only concerned about their own carbon emissions but are also stepping up to focus on the value of leading their ecosystem partners in carbon reduction. For some companies, the carbon reduction they lead may even exceed their own generated emissions, though this part of the reduction cannot be used to offset their own emissions, it deserves recognition and material and spiritual incentives, such as:

- Developing into CCERs or local inclusive CERs, converting into tangible economic benefits;

- Receiving tax incentives or fiscal subsidies (depending on local governments, but given that local governments have dual carbon targets, providing tax incentives or fiscal subsidies to high-quality carbon-reducing enterprises within their jurisdiction is not out of reach);

- Applying for the People's Bank of China's carbon reduction tool benefits (which is currently feasible);

- Winning titles for high-quality carbon-neutral enterprises awarded by the state, showcasing highlights of Chinese enterprises in the field of carbon neutrality at important platforms such as the UN Climate Conference, etc.

Previous articles have mentioned how companies in different industries (with a focus on consumer goods, technology, and finance) encourage their ecosystem partners to participate in carbon reduction actions, for example:

- Consumer brands enhance communication with consumers on issues of carbon neutrality and sustainability by disclosing the carbon footprint of their products, winning the favor of new consumers;

- Tech companies promote user participation in carbon reduction activities through carbon accounts. Currently, at least BAT (Baidu, Alibaba, Tencent) have launched their own carbon account products, achieving notable influence;

- Financial institutions (such as investment firms, banks, insurance companies, etc.) engage invested enterprises and customers in carbon reduction efforts, promoting overall carbon neutrality within the ecosystem. For instance, Temasek announced it will achieve 50% portfolio carbon neutrality by 2030 and 100% by 2050; Hillhouse Capital achieved its own institutional carbon neutrality in 2021 and will push numerous invested enterprises to achieve carbon neutrality.

The team recently participated in the construction of personal carbon accounts for many companies (including Goldwind, China Construction Bank, Microsoft, etc.), accumulating some insights and reflections:

- The biggest challenge in building a carbon account lies in identifying monitorable carbon reduction scenarios. With these scenarios, there is a possibility to generate carbon reduction points, and linking to external public scenarios (such as recycling clothes, clean plate check-ins, shared bicycles, etc.) can quickly enrich a company's carbon account scenes, launching a meaningful and engaging carbon account that allows employees and users to deeply participate.

- Currently, most carbon account scenarios are based on what people do not do or replace high-carbon scenarios to generate carbon points, but few explore "what to do" to generate carbon points. Perhaps many know that some gyms can convert the kinetic energy from treadmills or bicycles into electricity, which is real power generation! If similar technologies were popularized, for example, during the New Year, I played six games of ball, and if the kinetic energy generated from playing could be converted into electricity through wearable devices or equipment and stored, one could gain economic benefits from the electricity itself, while also generating clean energy, allowing a coal-fired power plant to produce less electricity, thereby reducing greenhouse gas emissions. There are already many such application scenarios now, such as Brazilian stadiums using football players' running to light up matches at night, and manufacturers have launched clothing that can convert running kinetic energy into electricity. If such technological products reach maturity and can be mass-produced, Carbonstop would be willing to be the first to invest. Imagine using the kinetic energy from running, cycling, and playing badminton to power real-life work and life; this will be true carbon inclusiveness and the most promising carbon account.

The Carbonstop team conducted an internal carbon account competition - Low Carbon With You - in Q4 last year, with very positive results, especially for new hires who gained deeper understanding and practical opportunities regarding carbon neutrality and low-carbon concepts through this activity. Generous rewards (five people received annual leave rewards from the company, and the winners of first, second, and third prizes won expensive Macbooks and iPads with disclosed product carbon footprints) and a team atmosphere where everyone participates were strong motivators for everyone to actively engage in low-carbon actions and carbon accounts. One of the carbon reduction scenarios in Low Carbon With You was linked to Fei Ant, China's largest recycled clothing platform, where employees could earn carbon points by recycling clothes, thereby increasing their chances of winning. In the end, one colleague donated over 100 kilograms of clothes they had accumulated over the years!

★ Offsetting (Offsetting):

Carbon offsetting is the final step for most companies to achieve carbon neutrality and is almost always necessary. Even if a company can ensure zero emissions from scope two by using entirely green energy, it is challenging to reduce emissions to zero in part of scope one and much of scope three by reducing direct energy consumption, consumption of high-GWP refrigerants, and through low-carbon purchasing behaviors. Therefore, unavoidable emissions are offset through carbon sinks or carbon reduction projects, which is also an internationally accepted paradigm for carbon neutrality.

I agree with Alibaba's approach that elimination is preferable to offsetting. If absorbing and capturing emissions directly through nature (such as forest carbon sinks) or carbon capture technology is feasible in terms of technology and economics, it will be prioritized for recommendation to companies.

However, an objective situation is that the cost of carbon sinks has risen significantly in recent years. Our team helped a company achieve carbon neutrality in the first half of 2021, when a tree planting organization quoted 40 yuan per ton of carbon sink capacity, but after less than half a year, the price had risen to more than 200 yuan. The reason given was that there are fewer places available for planting trees, and the operational costs of tree planting are getting higher.

China generates about 10 billion tons of carbon emissions annually, and forest carbon sinks can absorb approximately 434 million tons per year, leaving a significant gap.Carbon becoming a scarce resource is a clear signal, and both mandatory carbon trading compliance for emission control companies and voluntary corporate carbon neutrality are making carbon reduction and carbon sink capacities increasingly scarce. The latest carbon prices in the EU carbon market are close to 100 euros per ton, setting a new record. There is still considerable room for growth in China's carbon prices. People often ask when is the best time to stockpile carbon; I believe now is probably the best time (although I also remind that, like all trading products, there are risks in the carbon market, and caution is advised).

[A Message to Investors in the Carbon Neutrality Field: Predictions for the Future of Carbon Neutrality]

Recently, I have frequently communicated with top investors interested in the field of carbon neutrality (for example, I had a very exciting discussion with Zhang Lei, CEO of Hillhouse Capital, about the future of China's carbon neutrality, his view being thatCarbonstop promotes global carbon neutrality through product carbon footprinting, while Hillhouse hopes to drive society towards carbon neutrality through investment, both can play a significant role, but the premise is a shared long-term recognition of the value of carbon neutrality), while newly entering investment institutions ask the most questions about the ultimate ceiling of the carbon circle industry.

Tsinghua University and CICC both predicted the cumulative investment in China's carbon neutrality last year, and the basic tone is thatcarbon neutrality is a gold track worth trillions of yuan. Governor Yi Gang of the People's Bank of China recently emphasized that China needs 2.2 trillion yuan in investments annually to reach peak emissions, totaling 22 trillion yuan over ten years; from peak emissions to carbon neutrality, it requires 3.9 trillion yuan in investments annually, amounting to 117 trillion yuan over 30 years. Combined, reaching peak emissions and carbon neutrality require 139 trillion yuan in investments. As the core entry point of this major track in carbon neutrality:carbon emission calculation and carbon management will undoubtedly become a gold track worth at least a trillion yuan.

What will be the core of carbon neutrality/carbon management in the future?Data is essential. Only with sufficient underlying data is it possible for companies to calculate and manage carbon emissions, find key pain points for emission reduction through data analysis, and target emission reduction efforts, making carbon neutrality truly viable on both technical and economic grounds. This data mainly includes two aspects:corporate carbon emission data and underlying carbon emission factor data.

- The more operational carbon emission data disclosed by companies in different countries and industries, the greater the value of benchmarking analysis through data, enabling comparisons with past performance, industry benchmarks, and identification of strengths, gaps, and areas for improvement.

- The other important data comes from underlying carbon emission factor data provided by the state and industry. For example, how much carbon footprint does a dish of braised pork generate? How much does an iPhone, a cup, or a chair generate? Carbon footprint may become an important disclosure indicator for products and a critical consideration for consumers when choosing products. When will carbon footprint become an important disclosure indicator for products?

Never underestimate the intensity and speed with which China can advance something. Looking at the recent low-carbon ignition ceremony at the Beijing Winter Olympics, the determination to do well determines its historical significance, and any future Olympics attempting a low-carbon ignition method will likely refer to the Beijing model.

Given China's determination to promote carbon neutrality, the recent development speed of carbon neutrality, and the extent of popularization among the masses, I believe the widespread adoption of product carbon footprinting should occur within two years. When should consumer brands and manufacturing companies start preparing? I believe the best time is now! Many leading consumer brands (such as Starbucks, KFC, Adidas, Allbirds, L'Oreal, Chanel, etc.) have already taken action, and some top shopping centers and e-commerce platforms are also actively promoting products with disclosed carbon footprints and carbon-neutral products.

Regarding whether consumers are willing to pay a premium for carbon reduction/carbon-neutral products, this has been a long-standing debate. A recent study by IBM Institute for Business Value (IBV) found that 91% of Chinese consumers are willing to choose more environmentally friendly but potentially more expensive transportation methods; 70% of Chinese consumers are willing to change their shopping habits to reduce environmental impact; 65% of Chinese consumers say they are willing to pay an average 35% premium for brands that take responsibility for sustainability and the environment.

On the issue of green premiums, my view is twofold: on one hand, I agree with Bill Gates that innovation should lower green premiums, making carbon-neutral products price-competitive or nearly so with conventional products, so that consumers are not penalized financially; on the other hand, raising consumer awareness of low-carbon consumption is crucial. Raising awareness is not just abstract; internet companies are willing to incur huge costs to change user behavior because they see the value in user loyalty and long-term benefits.

If low-carbon consumption makes consumer brands, shopping malls, and e-commerce platforms see profit potential, it represents an opportunity for them to enhance competitiveness and win new consumer competition. In that case, the development of low-carbon consumption will certainly be faster and better than expected!

Many people think that carbon accounting is very similar to financial accounting. I partly agree and partly disagree. I agree that both carbon accounting and accounting involve data management, but I disagree that carbon emissions are only data. Carbon is also an asset. Currently, one ton of carbon is about 60 yuan per ton in China's national carbon market, and it has the potential to approach world carbon prices, such as the current 100 euros per ton in the EU. Companies doing good carbon accounting can guide targeted carbon reduction actions, and saving one ton of carbon is equivalent to earning dozens or even hundreds of yuan, which is the biggest difference from financial accounting.

In addition to the underlying data in the process of advancing carbon neutrality, a very important aspect is the allocation and certification of carbon emissions. Responsibilities for emission reductions need to be clearly defined between nations, enterprises, and individuals. Only when each country, company, and individual clarifies their carbon reduction targets and responsibilities and effective incentive measures are put in place, can people leverage their initiative, and carbon neutrality will have a real chance of being achieved.

According to IBV's perspective, capital will move away from carbon-intensive companies with high policy risks and low technological maturity, and the gap between these high-emission companies and low-emission ones will gradually widen. This will change the competitive foundation of every industry and steepen the cost curve for each product. According to IBV's survey of over 2,000 Chinese consumers in March 2021, 58% of individual investors have already considered "environmental sustainability" as a very important factor when choosing investment products.

People often ask what the most promising industries in the future of carbon neutrality will be? What struck me deeply is new energy vehicles, plant-based meat, recycled plastics, and other emerging industries, which can disrupt paradigms of clothing, food, housing, transportation, and use that humans have formed over hundreds or even thousands of years. The most exciting technology for me should be the direct generation of energy through everyday activities of each individual (such as running, cycling, playing badminton, etc.). This will mobilize an inexhaustible supply of energy throughout society and is closely related to each of us. I believe that only an industry that strongly connects with everyone has a truly vibrant life.

Although carbon neutrality is currently still in a period of rapid ascent, investment institutions must also recognize that, like any industry, carbon neutrality has its inherent volatility and cyclical patterns. The ability and success rate of a company to navigate through cycles determine how high and far the company can go in this race. The greatest driving force for a company to navigate through cycles comes from the company's original intention, mission, and team.

[A Message to Friends of Carbonstop (Partners, Clients, and Future Investors)]

Since its founding in March 2011, Carbonstop has undergone more than a decade of accumulation and sediment, experiencing several cycles in the carbon sector. It has never forgotten its original aspiration: “let every product have a carbon footprint,” and has set phased goals to “make carbon data ubiquitous, visual, and valuable!”

A grand and clear vision coupled with down-to-earth execution is the foundation upon which the Carbonstop team builds its future. Carbonstop will continue to empower enterprise clients to achieve carbon neutrality with technology, data, and expertise as its core drivers.

In 2021, Carbonstop focused its services on four major sectors: technology, consumption, finance, and energy. If further focus is needed in 2022 and only one of the four key sectors can be chosen, it will definitely be “Grand Consumption.” This strategic choice is based on Carbonstop's original mission and its core competencies.

After nearly a decade of accumulation, Carbonstop has built a database of nearly 150,000 carbon emission factors, which, in terms of quantity and coverage, has become the world's first, serving as the infrastructure for carbon emission calculations for companies across various industries. Recently, many universities have sought support from Carbonstop's carbon emission factor database to complete their research, and Carbonstop is honored to be involved, hoping that our work can contribute a small force to the progress of social carbon neutrality!

The construction of the carbon emission factor database faces numerous challenges, including finding authoritative domestic and international carbon emission factor data sources, but more importantly, actively discovering and independently calculating the carbon emission factors needed by various sectors of society. For example, the Carbonstop team took the initiative to calculate the carbon footprint of China's eight major cuisines, taking braised pork as an example, requiring the calculation of the carbon footprint of raw materials such as pork belly, star anise, spices, sugar, oil, and salt, as well as the carbon emissions from natural gas or electricity consumed during cooking. Finally, it is also necessary to consider the carbon footprint generated by the average waste handling (landfilling, incineration, etc.) of a dish of braised pork, averaging out to 6.22 kg of carbon footprint for a dish of braised pork for two people! More data can be queried in the 'Carbon Emission Factor Database' module of the 'Carbon Intelligence Hub' mini-program.

The construction of the database has made a significant leap from zero to one. Moving forward, there will be a greater emphasis on the power of technology and a collaborative, win-win approach to build a credible, applicable, and socially valuable underlying database together with like-minded individuals, contributing to the global realization of carbon neutrality.

Since its launch on September 22, 2021, Carbonstop's core SaaS product, Carbon Cloud, has received positive feedback from the industry, including positive affirmations from Dow Chemical, Porsche, Donghua University, Starbucks, KFC, SKP, Zhenggu, Beijing Jiaotong University, and other enterprises and institutions.

In 2022, Carbonstop will focus fully on solidly developing SaaS products to help enterprises and institutions conduct corporate carbon accounting, product carbon footprint calculations, full-process services for green meetings, and carbon account construction more efficiently, cost-effectively, and with lower barriers to entry.

Gradually stepping out of the red ocean market, focusing on SaaS for carbon management, standardized software, and in-depth consulting with strong professionalism and technological content is the starry sky and vast sea for Carbonstop! Believe in the power of focus!

[An Imagined Vision of a Carbon Neutral Company]

Imagine what our ideal carbon-neutral company looks like in 2022. I will describe my thoughts, hoping that looking back in the future, these can be realized, and I believe we can do even better then!

- The company's daily operational energy supply is pure renewable energy (preferably with a portion coming from the conversion of kinetic energy generated by employee movements);

- The office adopts facilities and measures such as sensor lighting, proactive architecture, and waste sorting (with clear traceability of waste disposal methods);

- Travel regulations stipulate that flights can only be taken for journeys exceeding three hours by high-speed rail;

- More than 80% of employees live near the company, minimizing commuting carbon emissions and conserving energy spent during travel;

- All company vehicles are electric vehicles;

- Through employee carbon accounts, each employee actively participates in carbon neutrality actions, understands the composition of their carbon emissions, and becomes an ambassador for carbon neutrality;

- Prioritize the procurement of carbon-neutral products and services (requiring suppliers to provide carbon neutrality reports or carbon emission reports);

- Prioritize carbon-neutral office buildings;

- Prioritize carbon-neutral data centers;

- Prioritize carbon-neutral investment institutions